Credit Card Rental Car Damage Coverage: How to File a Claim

How credit card rental collision coverage works — the decline-the-waiver condition, primary vs. secondary coverage, notice deadlines — and the step-by-step filing process with the document checklist administrators require.

How does credit card rental damage coverage actually work?

Card networks and issuers attach an auto rental collision benefit to many cards: if a rental car you paid for with the card is damaged or stolen, the benefit reimburses covered costs. The conditions are strict and nearly universal. You must decline the rental company's collision damage waiver at the counter — accepting the CDW/LDW usually voids the card benefit entirely — and pay for the full rental with the covered card. The benefit covers the rental vehicle itself: repair, theft, and often reasonable towing. It does not cover liability to third parties, injuries, or your belongings.

Exclusions vary by program and matter: certain vehicle classes (commonly trucks, some SUVs, exotic and antique cars), certain countries, and rentals beyond a maximum length are typical carve-outs. The controlling document is your card's guide to benefits — a PDF your issuer provides — and it, not this article, defines your coverage.

What is the difference between primary and secondary coverage?

Secondary coverage — the common form — pays after your personal auto insurance: the administrator asks what your insurer covered and reimburses the remainder, typically including your deductible. The practical cost is that your own policy gets involved, with whatever claims-history consequences follow. Primary coverage — a feature of some premium cards — pays without touching your auto policy, which is why frequent renters prize it. If you have no personal auto policy at all (city dwellers renting occasionally), secondary coverage generally functions as primary for the rental.

Check three things in your guide to benefits before you ever need them: primary or secondary; the coverage ceiling and rental-length limit; and the exclusion lists for vehicles and countries. Five minutes of reading before a trip beats discovering an exclusion inside a claim.

What is the step-by-step filing process?

- Locate the administrator: the guide to benefits names the claims administrator and contact — it is a benefits processor, not your issuer's customer service line.

- Open the claim immediately after damage occurs or a demand letter arrives — notice windows are often roughly 30–45 days, and opening costs nothing while waiting can forfeit everything.

- Get the claim number and the administrator's document checklist.

- Collect the rental company's paper: the demand letter, itemized repair invoice or estimate, and any inspection report — administrators expect you to request these, and rental companies are accustomed to providing them for card claims.

- Submit your side: rental agreement (all pages, showing the waiver declined), card statement with the rental charge, photos, police report if applicable.

- Track to resolution: respond to follow-up requests promptly; the administrator settles with you or directly with the rental company.

What documents will the administrator require?

The checklist is remarkably consistent across programs:

| Document | Notes |

|---|---|

| Rental agreement, all pages | Must show the CDW/LDW declined and you as driver |

| Card statement | Proves the covered card paid for the rental |

| Demand letter / damage notice | The rental company's claim against you |

| Itemized repair invoice or estimate | Flat amounts without itemization stall claims |

| Photos of the damage | Yours and the rental company's, labeled |

| Police report | Where an accident, theft, or vandalism occurred |

| Fleet utilization log | Commonly required before loss-of-use fees are reimbursed |

| Your insurer's decision | Secondary coverage only |

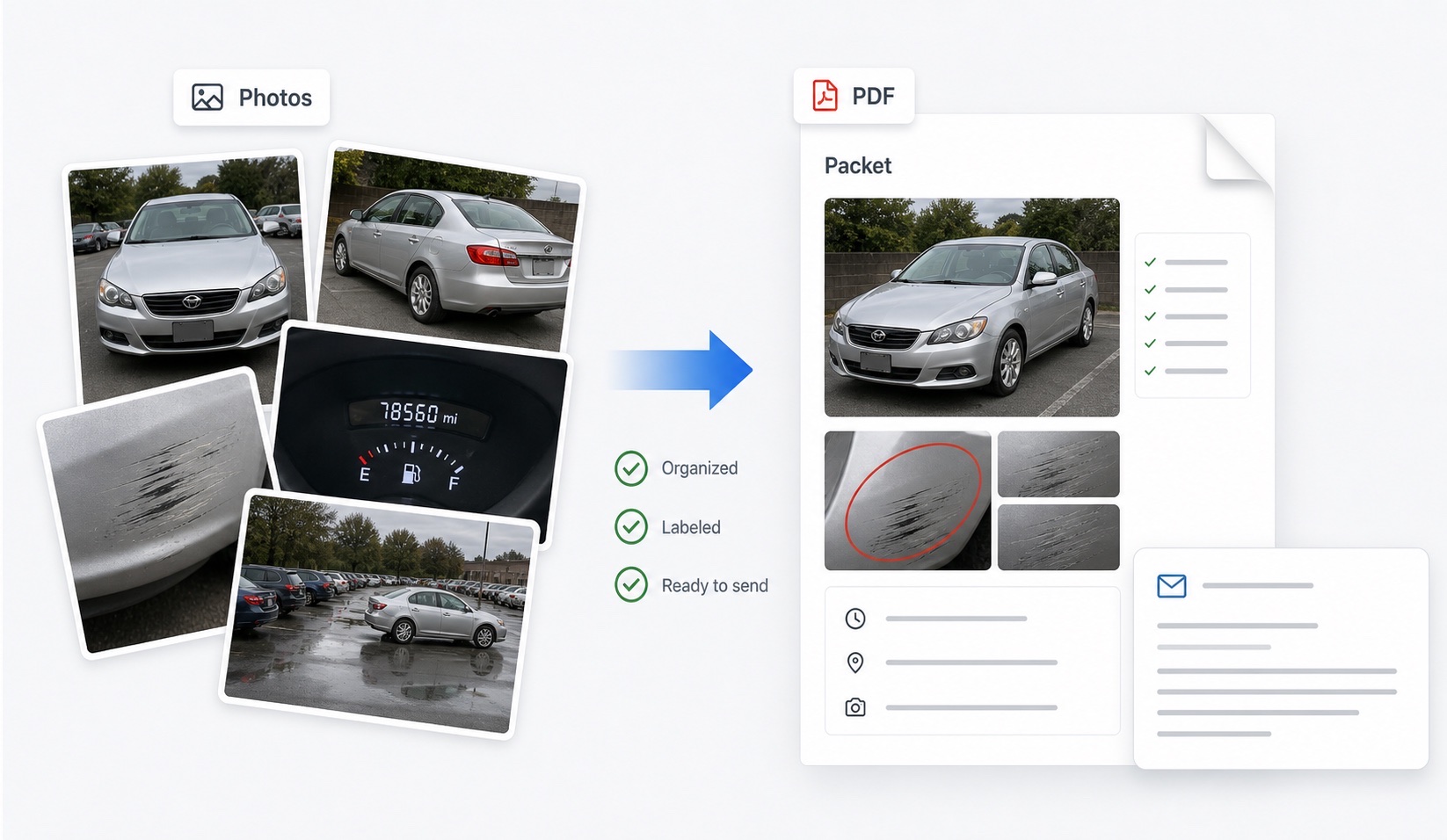

Present photos as a labeled before-and-after packet with a one-page cover note — the format DamagePacket exports — so the administrator matches evidence to demand lines without correspondence cycles. Keep originals of everything.

How does the card claim interact with disputing the charge?

Run both tracks in parallel, and say so in each. Disputing the rental company's claim (the evidence guide) attacks whether you owe anything; the card claim ensures that whatever survives the dispute is reimbursed. Open the card claim inside its notice window even if you expect to win the dispute — a dispute that fails at day 50 has already missed many programs' notice deadlines. Tell the administrator the charge is disputed; administrators handle this routinely and their own document demands to the rental company often surface the substantiation your dispute requested.

Two cautions. Do not pay the rental company's add-on fees uncritically expecting reimbursement — loss-of-use without a utilization log and unexplained administrative fees are exactly where programs push back, and where your dispute should too (fee guide). And keep the FCBA billing-error dispute distinct in your mind: that 60-day statement-based process addresses billing errors with your issuer, and is neither the rental benefit claim nor a substitute for it.

FAQ

How do I file a rental damage claim with my credit card?

Find the benefit administrator's contact in your card's guide to benefits, open the claim promptly after the damage or demand letter, then submit the requested file: rental agreement, card statement showing the rental payment, the rental company's demand and repair invoice, photos, and any police report. The administrator coordinates directly with the rental company from there.

What conditions must be met for card rental coverage to apply?

Almost universally: you declined the rental company's collision damage waiver (CDW/LDW) at the counter, paid for the entire rental with the covered card (or its rewards), and are a named or authorized driver. Coverage also typically excludes certain vehicle types, some countries, and rentals beyond a maximum length.

How fast do I have to notify the card benefit administrator?

Quickly — many benefit guides require notice within roughly 30 to 45 days of the incident, even though full documentation can follow later. Open the claim as soon as a damage demand arrives, including while you are still disputing the charge with the rental company.

Does card coverage pay loss-of-use and administrative fees?

Often only conditionally. Many programs reimburse loss-of-use only when the rental company produces supporting documentation such as a fleet utilization log, and treat administrative fees per the benefit guide's terms. Forward every fee line to the administrator rather than paying add-ons unexamined.

Is credit card rental coverage the same as liability insurance?

No. Card rental benefits generally cover damage to or theft of the rental vehicle itself. Liability for injuries or damage to other people's property is excluded — that protection comes from your auto policy, the rental company's liability coverage, or separate policies.