Rental Car Damage Claim Weeks After Return: Can They Do That?

A damage claim arrived weeks after you returned the rental. Whether that is allowed, why late claims are structurally weaker, the intervening-rental question that decides them, and how to respond without missing coverage deadlines.

Is a damage claim weeks after return even allowed?

In most cases, contractually, yes. Rental agreements typically authorize the company to charge for damage attributed to your rental after return, and few impose a short self-deadline for doing so. Late notices arise from real workflow: cars inspected at cleaning rather than at the return lane, damage surfacing at a later checkout, repair shops finding more once panels come off, and claims departments processing files in batches. So the arrival date alone does not invalidate the claim.

What the delay does do is shift the evidentiary weight. A claim raised at the return lane rests on a fresh inspection with you present. A claim raised three weeks later rests on the company's ability to reconstruct — with documents — where the damage came from across a window in which you had no control of the car. That reconstruction is exactly what your dispute should demand, item by item.

Why are late claims structurally weaker?

Because attribution decays with time and use. After your documented return, the car passed through employee hands (shuttling, cleaning, refueling), sat in lots among moving vehicles, and — the decisive factor — may have been rented to other customers. Every one of those exposures is an alternative source for the damage, and none of them is yours. The industry norm cited by consumer advocates is blunt: damage found after an intervening rental cannot fairly be pinned on the earlier renter, because the later renter received the car documented (or assumed) clean.

Your dispute makes this concrete with two timestamps and one question. Timestamp one: your return, fixed by the receipt or closed-contract email. Timestamp two: the damage's first documented recording — not when the letter was sent, when the damage was found. The question: what happened to the vehicle in between? Force all three onto the written record and the claim must defend its weakest ground.

What should I do in the first 48 hours after a late notice?

- Preserve the notice and its arrival date — the gap between damage discovery and notification is itself worth noting.

- Reconstruct your return: receipt or closed-contract email, return photos if you took them, and incidental timestamps (fuel receipt near the lot, parking stamp, boarding pass).

- Open coverage clocks: notify your card benefit administrator if the waiver was declined and a covered card paid (filing guide), and your insurer if it could be exposed — their deadlines run regardless of the company's lateness.

- Do not pay or accept quick-settlement discounts before substantiation.

- Send one written dispute with your evidence attached and the document demands below.

- Start the correspondence log: every message, dated, in one folder.

What documentation should I demand about the gap?

Aim every request at the window between the timestamps:

| Request | What it forces into the open |

|---|---|

| Date the damage was first documented, and by whom | The real length of the attribution gap |

| Dated, timestamped photos of the damage | Whether discovery matches the claimed date |

| Return inspection report from your drop-off | Whether any baseline was recorded when you left |

| Complete rental and movement history since your return | Intervening renters, shuttles, and lot time |

| Itemized repair invoice | Whether the amount reflects performed work |

| Loss-of-use and fee calculations | The add-ons that inflate late claims (fee guide) |

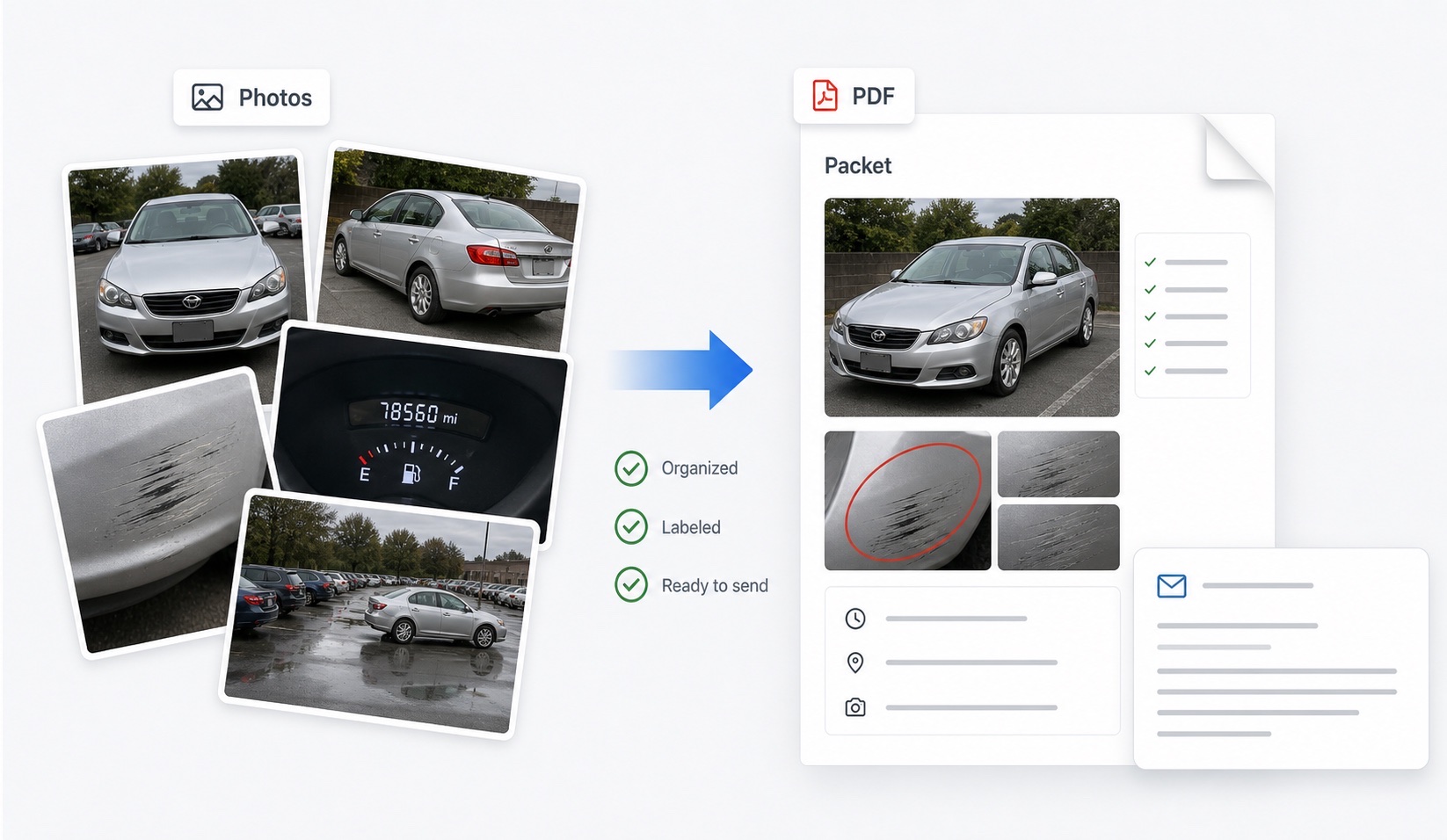

Pair the demands with your own packet — return photos matched to pickup photos by panel, receipt timestamps, the agreement — assembled as one labeled document (DamagePacket's before/after packet format, or a manual equivalent) so your side of the timeline is effortless to verify.

How do late-claim disputes usually resolve?

On substantiation, and often quietly. If the company's records show the car went out to another renter before the damage was documented, well-run claims departments close the file when the fact is put to them in writing — defending the attribution is untenable. If no return inspection exists and discovery was late, the claim rests on an undocumented baseline, and your dispute should say so plainly: nobody recorded the car's condition at hand-back, and the company's own process created that gap, not you. Claims also commonly shrink to the documented repair amount as the add-on fees fail their own paperwork.

If the company holds firm without producing the rental history or inspection dates, escalate on the record: supervisor review, the card administrator's parallel demands, state consumer protection complaints, small claims where money was already taken. And for every future rental, the five-minute return photo routine plus a saved receipt converts any future late claim from a negotiation into a lookup. The after-return dispute guide covers the full response mechanics.

FAQ

Can a rental company claim damage weeks after I returned the car?

Usually yes, contractually — most rental agreements authorize damage charges after return with no short internal deadline. But a late claim must still be substantiated, and the weeks between your documented return and the damage's documented discovery are the claim's structural weakness, not yours.

Does a late damage claim mean the company is scamming me?

Not necessarily — delayed inspections, repair-shop discoveries, and slow claims processing produce honest late claims. But lateness legitimately raises the attribution question: the longer the gap, and the more the car was used in it, the weaker the link between you and the damage. Ask for the dates and rental history in writing.

What is the single most important question to ask about a late claim?

Whether the vehicle was rented to other customers between your return and the date the damage was first documented. If it was, the damage cannot be cleanly attributed to your rental, and you should ask the company to explain the attribution on the record.

Do coverage deadlines still apply if the claim itself was late?

Yes, and this is the trap: credit card benefit notice windows (often roughly 30–45 days) and insurer reporting requirements run from when you learn of the claim or incident. Open coverage claims immediately upon receiving a late notice, even while disputing it.

What if I no longer have my photos from the rental?

Rebuild the timeline from what remains: the return receipt or closed-contract email, card statements, fuel and parking receipts, and the company's own checkout report. Then demand their records — a late claim with no documented baseline on their side has the same evidence gap they would hold against you.